Updated: 11/09/2024

You know how people can get fired up over whether Coke or Pepsi is better? Well, that’s basically what’s going on with ETFs vs. index funds. Some investors are so passionate about which one is “better,” they’ll defend their choice like it’s the last soda on earth. But here’s the twist—the difference between ETFs and index funds might not be as big as everyone makes it out to be, especially when you’re chasing FIRE (Financial Independence, Retire Early).

Imagine this: You’re standing at a fork in the road. One path is labeled ETF, the other Index Fund. Both look equally promising, but which one should you take? Should you spend your time trying to figure out which is “better,” or could this debate be much ado about nothing?

Spoiler alert: It’s not about which one is better—it’s all about strategy. That’s the secret sauce. Whether you sip Coke, Pepsi, or neither, the important thing is having a plan that works for you and sticking with it. When it comes to FIRE, it’s about consistency and sticking to a long-term strategy, not getting bogged down by the technical differences between these two investment tools. Let’s break it down.

What Are ETFs and Index Funds?

Let’s start by unpacking what these two mysterious acronyms actually mean. First up—ETFs, or Exchange-Traded Funds. Think of them as baskets of stocks or bonds that you can buy and sell throughout the day, just like individual stocks.

Imagine walking through a farmer’s market where you can pick up a basket filled with a variety of fruits (or stocks, in this case). The cool part? You can trade these baskets in real-time, with prices fluctuating throughout the day as the market bounces up and down. It’s like getting that instant feedback you crave—whether good or bad—every time you peek at your brokerage account.

On the other hand, index funds are more like mutual funds that aim to replicate the performance of a specific market index, like the S&P 500. Instead of trading throughout the day, index funds are priced only once—at the market’s close. So, when you invest, you won’t know the exact price you’re getting until the end of the day.

Think of it as ordering dinner at a restaurant, but you don’t get to taste it until the kitchen closes. It’s a bit less reactive and more hands-off, perfect for those who prefer a slower-paced approach to their investments.

Key Differences Between ETFs and Index Funds

Trading and Pricing

When it comes to ETFs, it’s all about that live-action thrill. Prices shift throughout the day, allowing you to buy and sell whenever the mood (or the market) strikes. This real-time pricing makes ETFs great for those who want to stay a bit more hands-on, keeping an eye on the market and maybe even doing a little day trading on the side. It’s the fast lane of investing.

In contrast, index funds are more like the scenic route. They have just one price, set at the end of the trading day. If you’re the kind of person who prefers to “set it and forget it,” index funds fit the bill. You place your order, walk away, and find out the price later—no need to stress over market fluctuations throughout the day. It’s a chill, long-term way to grow your wealth.

Now, let’s talk about how much of a slice you can get. ETFs often let you buy fractional shares, meaning you don’t need to shell out for a full share if you’re just dipping your toes in. Want to invest but don’t have hundreds or thousands to spend? No problem—you can buy a small piece of the ETF pie.

With index funds, though, it’s usually a whole-share situation. You might need to buy the full pie rather than just a slice, though some platforms are starting to offer fractional shares for index funds as well. Historically, this has made ETFs a more flexible option for smaller investors.

Minimum Investments

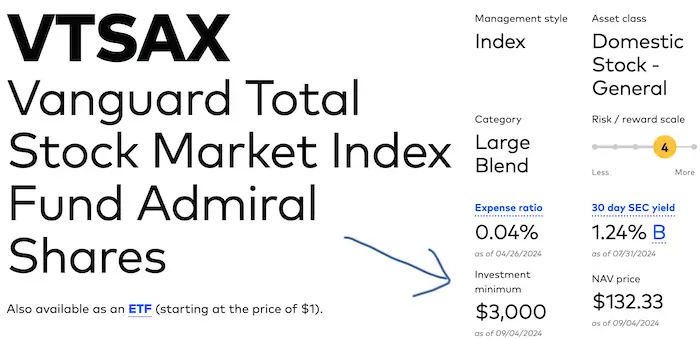

One of the biggest sticking points for new investors can be minimum investments. ETFs generally have no minimum requirement aside from the cost of a single share. It’s a come-as-you-are vibe, making ETFs super accessible for beginners.

On the other hand, index funds often have a minimum investment—sometimes as high as $3,000 to get started. That’s been a barrier for some, though many brokers are lowering these minimums or even doing away with them entirely. So, while index funds might feel like the fancier option with a dress code, that’s slowly changing as well.

VTI vs. VTSAX: Different Vehicles, Same Destination

Let’s break it down. VTI and VTSAX are like two different cars driving you to the same destination. Both track the Total Stock Market Index, meaning whether you go with the VTI ETF or the VTSAX index fund, you’re getting exposure to the entire U.S. stock market—the whole enchilada of stocks, from the largest companies down to the smallest.

But here’s the twist: despite their different formats, their core exposure is identical. Both are designed to mirror the performance of the entire U.S. stock market, so it’s less about what’s inside and more about how they operate.

- VTI (the ETF) gives you the flexibility of real-time trading and fractional shares, perfect for those who want to stay nimble.

- VTSAX (the index fund) offers that end-of-day pricing and is often the go-to for long-term investors who prefer a slower, steadier approach.

For us, VTI just clicks. Maximizing our savings into VTI was one of the steps to our $1 Million Early Retirement.

We’ve chosen Schwab Brokerage because it aligns with our strategy of keeping fees low, offering ease of use, and allowing for a lot of flexibility without needing a high minimum investment. With VTI, we can stay consistent with our investments, focus on the long term, and let compound growth do the heavy lifting.

In the end, the choice between VTI and VTSAX is less about which is better and more about which style suits your approach. For us, VTI fits like a glove—but both get you where you want to go.

Why Strategy Matters More Than Semantics

At the end of the day, the whole ETF vs. index fund debate is like arguing over Coke vs. Pepsi—sure, there are differences, but they pale in comparison to the bigger picture. When it comes to reaching financial independence and retiring early (FIRE), what really matters isn’t whether you pick VTI or VTSAX, but whether you stick to a solid investment strategy.

It’s easy to get caught up in the technical details—real-time trading vs. end-of-day pricing, fractional shares vs. whole shares—but here’s the truth: these are small fries. The real secret sauce to achieving FIRE is consistency and discipline. Whether you’re team ETF or team index fund, what will truly drive your success is regular investing, keeping your costs low, and staying the course, especially when the market gets rocky.

Both ETFs and index funds are just tools. It’s how you use them that counts. Instead of sweating the small stuff, focus on the bigger game plan: save diligently, invest regularly, and stick to your plan. Over time, the power of compounding will do the heavy lifting for you. The right strategy, paired with consistency, beats obsessing over the fine print every single time.

Lessons From Our Personal Journey

Jason’s Early Mistakes

When I first dipped my toes into investing, I was all over the place. I made the classic rookie mistake of thinking I could outsmart the market—buying individual stocks, trying to time my trades just right, and endlessly stressing over every little decision. Should I choose an ETF or an index fund? Should I invest in this hot new stock or stick with what I know? Spoiler alert: none of it worked out the way I hoped. Trying to predict the market is like trying to predict the weather—you might get lucky once, but most of the time, you’re just chasing your own tail.

I was laid off at 31. Here’s learn what I did next.

The Bigger Picture

What I eventually learned is that the details don’t matter as much as you think. The real magic lies in focusing on the bigger picture—building a strategy and sticking with it. Whether I chose an ETF or an index fund ended up being far less important than staying consistent with my investments and not freaking out every time the market dipped. My success didn’t come from perfect timing or picking the right individual stocks; it came from trusting the process and letting time and compounding do their thing.

If there’s one takeaway from our journey, it’s this: don’t let the small stuff distract you. Whether it’s VTI or VTSAX, the key is to keep investing, stay the course, and focus on the long-term. That’s what truly leads to financial freedom—not agonizing over which investment vehicle is marginally better.

Conclusion

At the end of the day, both ETFs and index funds are excellent tools for building wealth and achieving financial independence. The key takeaways are simple but powerful:

- Keep your costs low – Whether you choose ETFs or index funds, minimizing fees will make a huge difference in the long run.

- Stay consistent – The secret to success isn’t timing the market or picking the perfect stock; it’s regularly investing and staying the course, even when the market gets bumpy.

- Focus on the long-term strategy – Build a plan that works for you, stick to it, and don’t sweat the small stuff.

The debate between ETFs and index funds might feel important, but the reality is that strategy and discipline will always trump semantics. So, keep learning, stay focused, and invest smartly. Whether you’re on Team ETF or Team Index Fund, the important thing is that you’re moving toward your goals.

I Was Laid Off at 31: How I Retired Early at 39

I Was Laid Off at 31: How I Retired Early at 39

Leave a Reply